When Tarun Loomba became chief executive of Mitel Networks Inc. in 2021, the company made an interesting pivot.

While the entire communications industry has been shifting to a software-as-a-service-based model, leveraging the public cloud, Mitel took a step back, looked at its strengths and the market, and decided to dedicate itself to serving customers via private or hybrid clouds.

Given the momentum around the public cloud, it was easy to look at Mitel’s decision as nothing more than head-scratching, but the reality is that customers want greater business outcomes veruss a delivery model conversation, and the public cloud isn’t always the right answer. Making the right choice of cloud architectures depends on understanding the outcomes the business desires. This, in turn, requires asking the right questions to meet those outcomes.

After the big push during the pandemic to digitize everything, the first technical question derived from the business outcomes is whether rapid provisioning is required or the need to scale up and down quickly. According to public sources, about 500 million office workers are thought to have this need. In addition to this, the addressable market for digital solutions among deskless workers is approximately 1.5 billion workers globally.

Businesses must choose the best architecture that meets their business needs, and this leads to one size that doesn’t fit all. Organizations with a mix of use cases, with a variety of privacy and security laws and requirements, will be better served with a mix of connected solutions and a hybrid implementation.

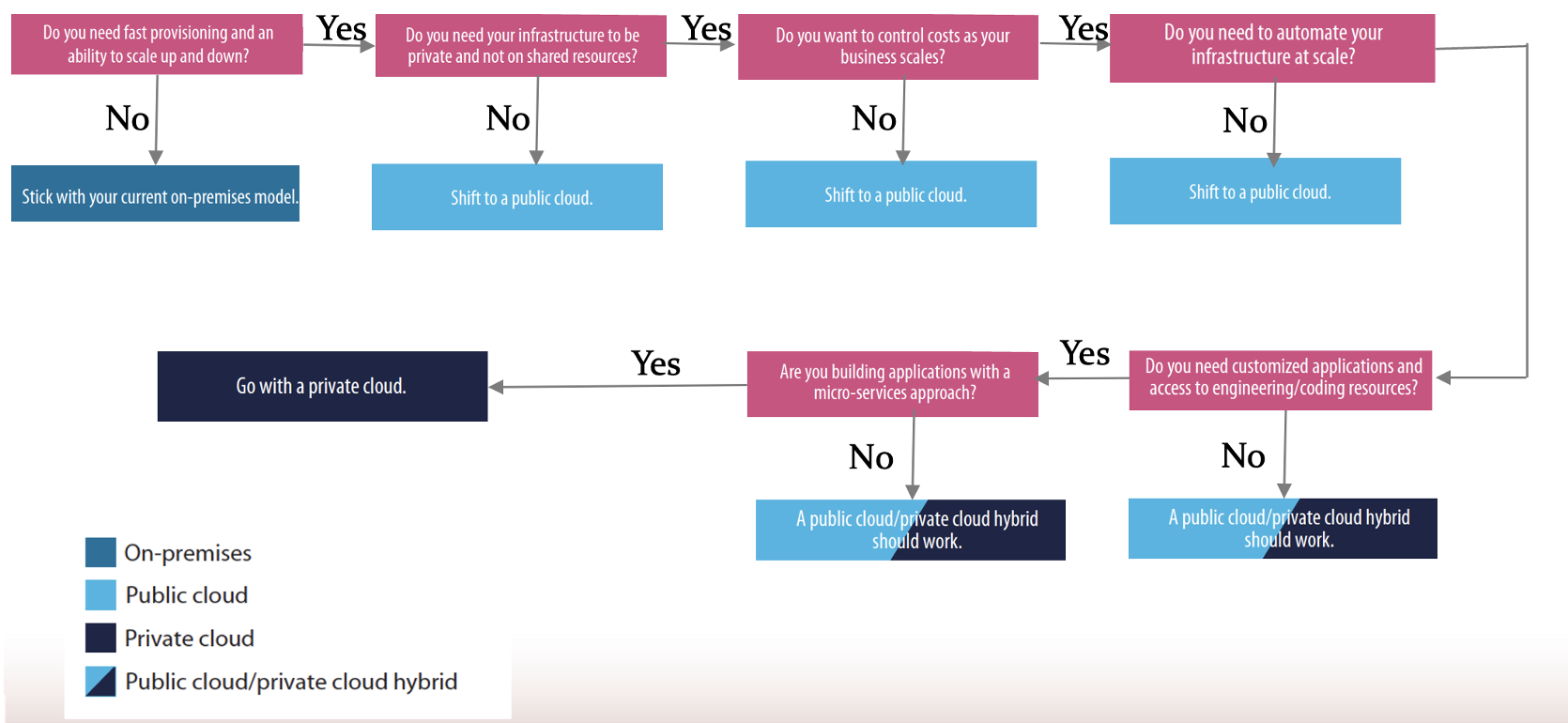

To help decision-makers, I have created a “cloud decision tree,” shown below. The flow can be followed, and business requirements can be mapped to technical requirements, which helps guide to the best cloud model. For example, the next question asks, “Do you need your infrastructure to be private and not on shared infrastructure.” Many businesses in regulated industries, such as healthcare and finance, would fall into this category.

If one follows the line of questions, many businesses will end up with a hybrid environment that leverages the strengths of public and private clouds. For those looking for proof of this, look no further than the hyperscalers and large SaaS vendors, as they all have their private cloud stacks to complement their public offerings.

I recall being at AWS re:Invent when the company rolled out its private cloud solution. In the analyst Q&A, I asked then AWS CEO Andy Jassy why the company chose to do that after being the poster child for public clouds for decades, and he explained, “It’s what our customers have been asking for.”

Most of the tech industry has embraced a hybrid cloud, but communications have changed slowly. This shouldn’t be a huge surprise, as communications has never been an early adopter. It was late to shift to internet protocol, to the cloud, to cloud-native and now to hybrid cloud.

I’m certainly not criticizing the communications industry. There’s a reason unified communications and the contact center have been late adopters to the cloud and not to hybrid multicloud. Phone systems, collaboration tools and contact centers are the most mission-critical of applications, and a down system means lost money. This is why communications teams often deal with an “If it ain’t broke, don’t fix it” mentality.

To date, cloud adoption in communications has been using a public cloud model, but that’s because organizations with more complex requirements stood pat until they could chart a path that cloud solve requirements such as data sovereignty customization and control over security. This is why most of the early adopters of unified communications as a service and contact center as a service were small to midsized businesses.

Looking ahead, I do expect UCaaS and CCaaS growth to continue to be strong, but I also expect to see a rise in private and hybrid cloud deployments as the cloud delivery model, regardless of where it is located, delivers greater agility and feature velocity and meets the needs of hybrid work better. For Mitel, this puts it in a unique competitive position. Given the erosion and shift in focus by the other traditional UC vendors, combined with Mitel’s shift in strategy to deliver innovation to UC, it is arguable that Mitel has never been in a better position to capture UC share, versus UCaaS.

I want to be clear: I’m not saying on-prem UC and private cloud will outpace UCaaS/CCaaS growth, but I believe the decline will be slower than most people expect as these technology transitions take a long time. Someone once asked me if I foresee a day when all communications are in the cloud, and my response was, maybe, but I’ll long be dead when that happens. Until then, Mitel can grow through innovation combined with the ability to take share from all the others that have exited and have moved to SaaS only.

Mitel’s focus on business outcomes supported by a mix of solutions for its customers’ high-value use cases will be the key to driving momentum and differentiating from the pure cloud-only providers. This is part of why Mitel’s strategy is so interesting. It puts customer outcomes in front of the debate over the type of deployment method. Mitel has committed to its strategy of focusing on UC and has evolved it by acquiring the Unify assets from Atos.

I’m also interested in seeing what Mitel’s new Chief Marketing Officer Eric Hanson brings to the table. Hanson comes to Mitel from cyber vendor OneSpan Inc., and before that, communications provider Fuze Inc., which was acquired by 8×8 Inc. He is an experienced marketing leader with deep knowledge of the communications market and seems to be experienced in driving go-to-market and brand awareness in the technology sector. This is what Mitel needs at this point in its history.

The bet Mitel made almost five years ago was certainly contrarian to the rest of the industry. But Mitel would not have survived being another “me too” UCaaS/CCaaS provider because its products were too far behind the massive number of competitors. Instead, it focused on its strengths. Now the industry pendulum is swinging back, and Mitel has found itself in a good position to use this as a tailwind.